Fact-checked against Services Australia — Medicare on 2026-04-25.

You’ve probably heard Australian healthcare called free. You’ve probably also heard people complain it cost them a fortune. Both can be true on the same day, in the same clinic. The reason is that costs here run on layers – Medicare rebates, gap fees, the PBS, the Safety Net, and private insurance – and what you actually pay for any given service depends on which of those layers happen to apply to you. “Free” and “expensive” aren’t contradictions. They’re just two different patients standing at the same reception desk.

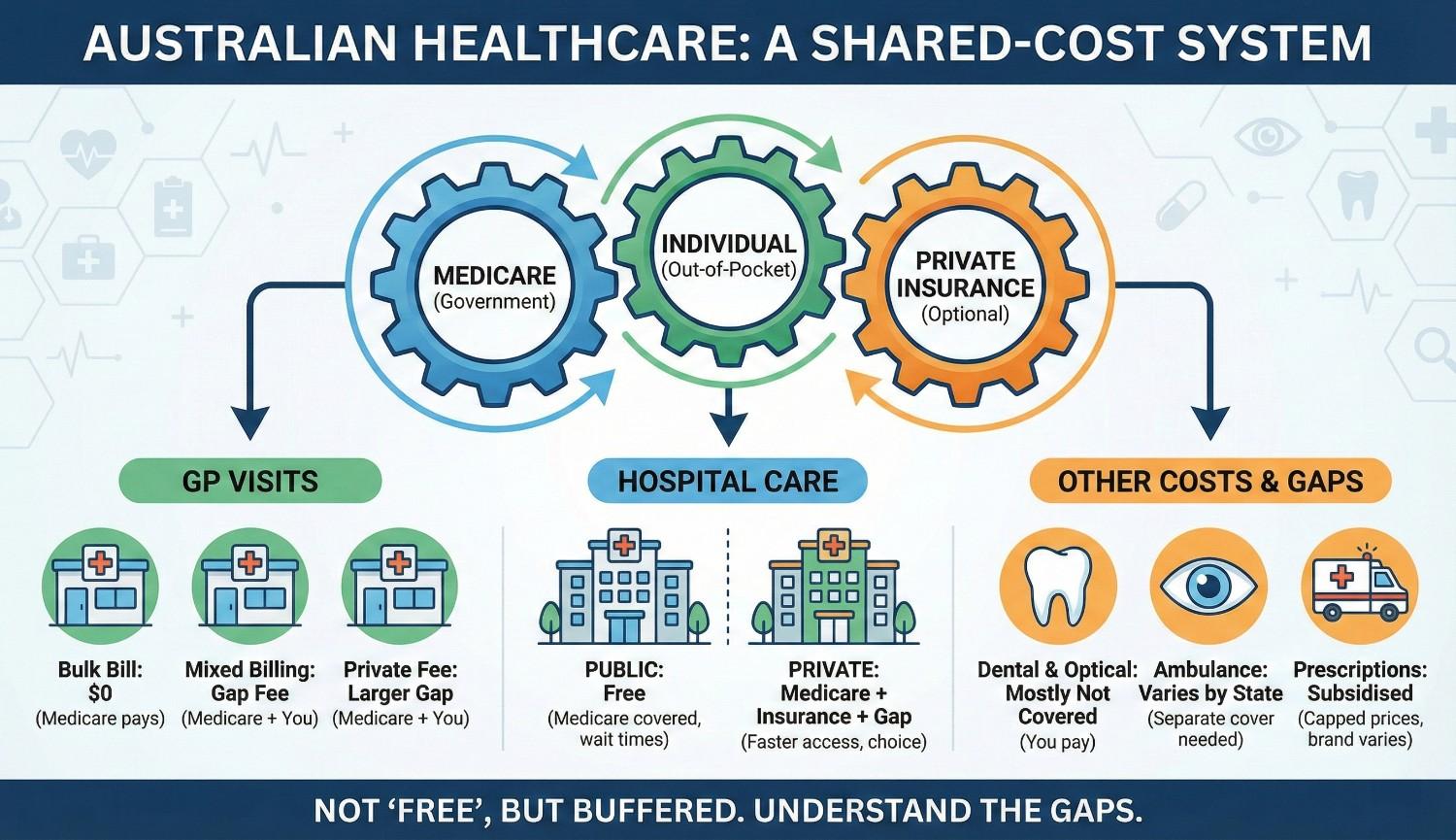

The four layers of healthcare costs

Nearly every healthcare cost in Australia is shaped by some mix of four layers. Once you can name the layer doing the work, most of the confusion drops away.

- Medicare rebates – the federal payment for medical services on the Medicare Benefits Schedule

- Provider fees – the amount the doctor, specialist, or clinic actually charges

- The PBS – federal subsidies for prescribed medicines on the Pharmaceutical Benefits Scheme list

- Private health insurance – optional cover that fills specific gaps the public system doesn’t

If you want the bigger picture – public hospitals, the federal-state split, where private cover sits in the whole structure – that’s in our healthcare system structure explainer. This article sticks to one thing: the costs you actually see in real care.

| Layer | What it pays for | Who controls it |

|---|---|---|

| Medicare rebate | Medical services on the MBS | Federal government |

| Provider fee | The doctor, specialist, or clinic’s charge | The provider |

| The PBS | Prescribed medicines on the PBS list | Federal government |

| Private health insurance | Hospital and extras gaps Medicare doesn’t cover | Your insurer (federally regulated) |

Medicare rebates and the schedule fee

Medicare doesn’t hand over a flat dollar amount per visit. It pays a set rebate per service, and every service has its own Medicare Benefits Schedule (MBS) item number. A short GP consult is one item number. A longer one is another. A specialist consult is something else again. For the authoritative version of how all this works, the Services Australia Medicare hub is the place to go.

Each item has a “schedule fee” attached to it. The Medicare rebate is a percentage of that fee – typically 85% for out-of-hospital services and 75% for in-hospital private treatment. Either you or the provider receives the rebate, and the gap between the rebate and what the provider actually charges is exactly where your out-of-pocket cost lives.

So two numbers decide the cost of any service: the MBS item number, which fixes the rebate, and the provider’s fee, which fixes the total. You feel the difference between them at the till.

Bulk-billing – what it is and isn’t

Bulk-billing simply means the provider accepts the Medicare rebate as full payment. You pay nothing on the day, and the provider bills Medicare directly for the rebate amount.

It isn’t a discount. It’s a billing model. A provider who bulk-bills has decided the rebate covers the service. A provider who doesn’t has decided it doesn’t, and charges you the difference. Same service, different call on whether the rebate is enough.

How often you’ll get bulk-billed depends heavily on the service:

- Standard GP consultations are commonly bulk-billed for concession-card holders, less commonly for general patients (and the rates have shifted in recent years)

- Specialist consultations are rarely bulk-billed

- Many diagnostic services (pathology, simple imaging) are commonly bulk-billed

- Higher-complexity diagnostic services (MRI, certain scans) are often not

The cheapest way to dodge an unexpected fee is to ask before you book. Reception staff will tell you straight whether the provider bulk-bills.

Gap fees and out-of-pocket costs

A gap fee is the difference between what a non-bulk-billing provider charges and what Medicare rebates back. Say a GP charges $90 for a standard consult and the Medicare rebate is around $42. The gap is roughly $48. You pay the full $90, then the rebate comes back to you – often instantly through electronic claiming.

Gap fees are common, and they’re legal. Providers set their own fees and Medicare doesn’t regulate them. The flip side is choice: a clinic charging more often gives you shorter waits, longer appointments, or specialist expertise you’ve decided is worth paying for.

Specialists are where gaps get bigger. A first specialist consult can leave you $100 to $200 or more out of pocket, depending on the specialty and where you are. When those gaps start piling up across a year, the Medicare Safety Net page at Services Australia explains what kicks in.

Worked example – a standard GP gap (illustrative only)

Using the numbers above, here’s how one non-bulk-billed visit breaks down. Illustrative only.

| Provider’s fee | $90 |

| Medicare rebate | about $42 |

| Your gap (out-of-pocket) | about $48 |

| Paid on the day | $90, with the rebate returned after |

The Medicare Safety Net

The Medicare Safety Net is the federal mechanism that brings your out-of-pocket costs down once you cross a set annual threshold. It’s there for exactly the situation where gap fees stack up – chronic conditions, frequent specialist appointments, families with high care needs.

There are two thresholds:

- Original Medicare Safety Net – once gap-fee spending hits the threshold, Medicare pays 100% of the schedule fee for further services (instead of 85%) for the rest of the calendar year

- Extended Medicare Safety Net – a higher threshold, after which Medicare pays a percentage of the gap above the schedule fee, capped at certain limits

Concession-card holders reach the thresholds at lower amounts. Families can register together so their spending counts as one pool.

One thing worth knowing: for an individual the Safety Net is automatic, because Services Australia tracks your spending for you. For a family, the pooling only happens if you register. Plenty of people miss a threshold they’d have crossed easily if their household spending had been counted together.

The PBS and prescription costs

The Pharmaceutical Benefits Scheme is the federal subsidy that brings down the cost of prescribed medicines. The about-the-PBS page walks through the listing process, the patient co-payment, and the safety net.

The mechanics are straightforward. Medicines on the PBS list carry a capped patient co-payment, with lower concessional rates for pension and healthcare card holders. Medicines that aren’t on the list are charged at full retail price, unless something else covers them – a private extras policy, say, or a specific subsidy.

Three things drive what you pay for a prescription:

- Whether the medicine is on the PBS list – listed medicines have the capped co-payment; unlisted medicines don’t

- Whether the patient holds a concession card – pensioners and healthcare card holders pay much lower co-payments on PBS items

- Whether the PBS Safety Net has been hit – once annual PBS spending reaches the threshold, further medicines are free or near-free for the rest of the year

If you’re on long-term medication, two habits save real money over a year: track your PBS spending toward the safety net, and ask your prescriber whether a PBS-listed alternative exists for anything you’d otherwise be paying full retail for.

Private health insurance and the gap

Private health insurance in Australia is regulated federally and runs alongside Medicare, not instead of it. For policy comparisons and the rules around the Medicare Levy Surcharge and Lifetime Health Cover loading, the federal portal at privatehealth.gov.au is the authoritative source.

Here’s what private cover changes about your costs:

- Hospital cover – pays the difference between Medicare’s in-hospital rebate (75% of the schedule fee) and the actual cost of private hospital treatment, subject to policy limits

- Extras cover – subsidises dental, optical, physio, and other services Medicare doesn’t cover, up to annual limits

- Tax effects – some higher-income earners pay the Medicare Levy Surcharge if they don’t hold appropriate private hospital cover

And here’s what it doesn’t change:

- Standard out-of-hospital GP and specialist gap fees – these are still paid by the patient in most cases

- PBS prescription costs – these are governed by the federal PBS, not private insurance

- Public hospital treatment – eligible patients still get this free as public patients regardless of private cover

And eligibility for Medicare itself – the foundation everything here sits on top of – is covered separately in our Medicare eligibility article.

Frequently asked questions

Why am I charged a gap fee at the doctor in Australia?

Gap fees happen when a provider charges more than the Medicare rebate amount. Medicare pays a fixed rebate per service (set by the Medicare Benefits Schedule); if the provider’s fee is higher, the difference is the patient’s out-of-pocket cost. Bulk-billing providers accept the rebate as full payment; non-bulk-billing providers pass on the difference. Right.

How does the Medicare Safety Net work?

The Medicare Safety Net reduces out-of-pocket costs once a patient or family hits an annual threshold. After the threshold is reached, Medicare pays a higher percentage of the schedule fee for out-of-hospital services for the rest of the calendar year. Two thresholds apply — original and extended — with concession-card holders crossing them at lower amounts.

Does private health insurance reduce gap fees?

It depends. Private hospital cover can reduce or eliminate gap fees for in-hospital private treatment, depending on the policy and the provider. Private extras cover subsidises out-of-hospital services like dental and physio that Medicare doesn’t cover. Neither type usually changes gap fees on standard Medicare-covered GP or specialist visits.

Where unexpected healthcare costs usually come from

The bills that catch people out rarely come from the obvious places. They come from three quieter ones: specialist gap fees that turn out far higher than the GP visits you were used to, prescriptions for medicines that simply aren’t on the PBS, and ambulance bills – which are state-level and not covered by Medicare at all. Every one of these is published somewhere; the rules sit on .gov.au sites. They’re just not the costs most people see coming.

What matters most – in order

If you’re managing healthcare costs over time, this is roughly the order of things worth doing:

- Know which layer applies to each service – Medicare rebate for medical services, PBS for medicines, private cover for hospital and extras, state systems for ambulance.

- Ask about gap fees before you book, especially with specialists.

- Register as a family for the Safety Net so your spending pools.

- Track your PBS spending toward the safety net through the year.

None of these moves is large on its own. Together, though, they’re most of the difference between the people who feel blindsided by healthcare costs and the people who don’t.