Fact-checked against Services Australia — Age Pension on 2026-04-25.

Most people think of the Age Pension as a safety net for the few. It isn’t. It’s the federal income-support payment for older Australians, and it does a lot more heavy lifting in retirement than people realise until a parent gets close to claiming. Almost two-thirds of Australians over Age Pension age draw at least a part-pension, and most of the rest sit just outside the means-test thresholds. So this isn’t a backstop on the edge of the system – it’s a core part of how most Australians actually fund their later years.

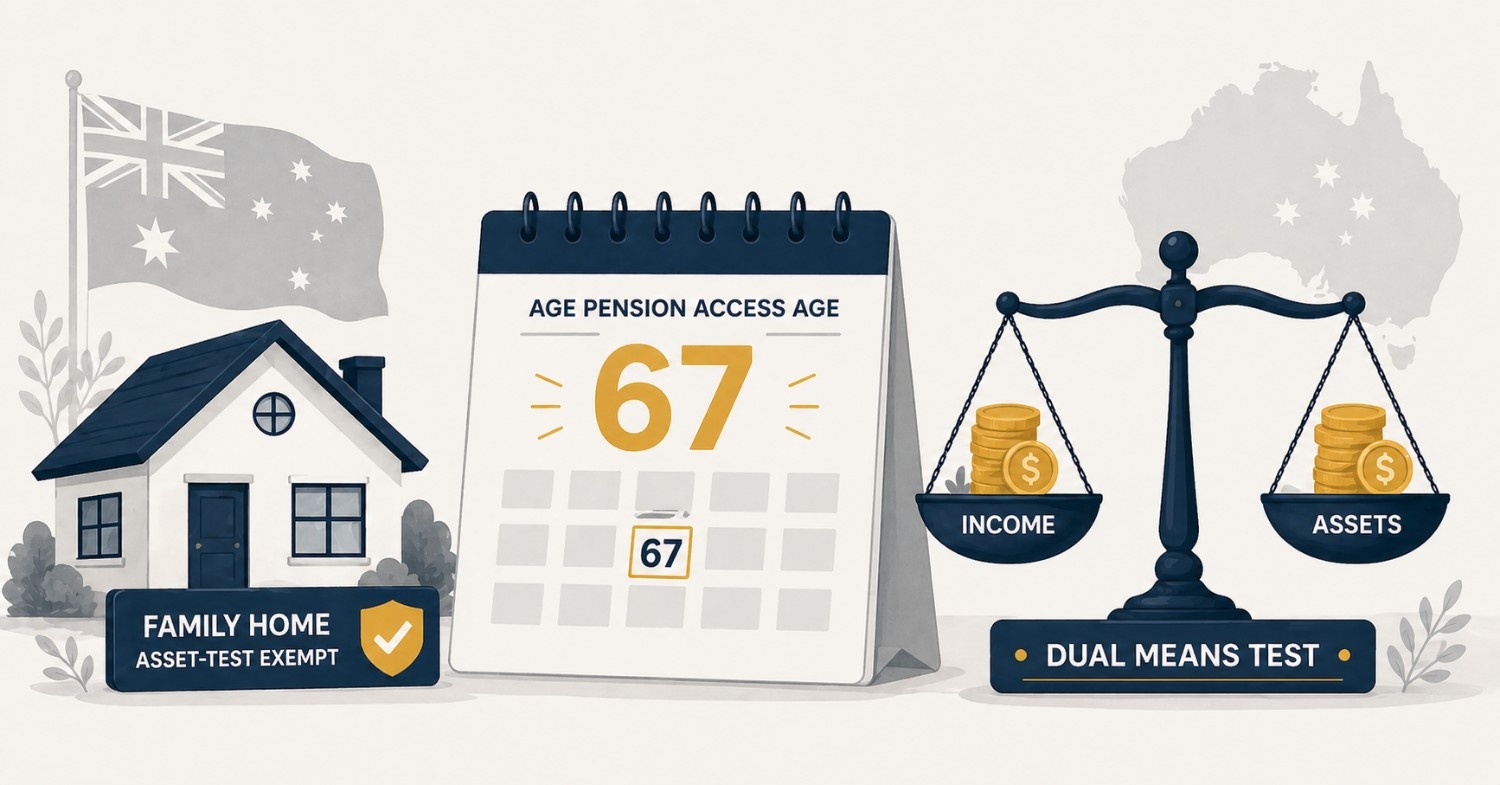

The three tests every Age Pension claim runs through

Every claim has to clear three separate tests. Pass two and fail one, and you still don’t get the full payment. All three matter:

- Age and residency – qualifying age and residency duration requirements

- Income test – how much income (including deemed income from financial assets) the person and partner have

- Assets test – how much in countable assets the person and partner hold

Here’s the part that trips people up. Services Australia runs both the income test and the assets test, then pays you on whichever one gives the lower result. So clearing the income test is no help if the assets test cuts you down – and vice versa. Both have to be navigated. The detail sits on the Services Australia income and assets tests page.

If you want the wider picture – who qualifies for Centrelink payments generally – that’s in our Centrelink eligibility article. This one stays focused on how the Age Pension itself is worked out.

| Test | What it measures | Must you pass it? |

|---|---|---|

| Age and residency | Whether you have reached qualifying age and met the residency duration | Yes – a hard gate |

| Income test | Your and your partner’s income, including deemed income from financial assets | Yes – the lower of the two means-test results is paid |

| Assets test | Your and your partner’s countable assets, with the family home exempt | Yes – the lower of the two means-test results is paid |

The qualifying age and residency requirements

The qualifying age for new claimants is 67. It climbed from 65 in steps over a published schedule, and anyone born on or after 1 January 1957 reaches Age Pension age at 67. You can check the table on the “when you can get it” page.

Hitting that age is only the first hurdle. Residency adds a second:

- Generally need to be an Australian resident at the time of claim

- Have been an Australian resident for a defined number of years (commonly 10 years total, with at least 5 years continuous)

- Some exceptions apply for people from countries with international social security agreements

If you moved overseas later in life, or migrated to Australia closer to retirement age, residency can quietly become the thing that holds up your claim. That’s exactly why it pays to understand it well before you reach qualifying age, not on the day you go to claim.

The income test in practice

The income test counts:

- Wages and salary, including casual work after retirement

- Business and self-employment income

- Deemed income from financial assets – Centrelink applies a deeming rate to bank accounts, term deposits, shares, managed funds, and (for new pensioners after 2015) account-based pensions

- Foreign pensions and overseas income, in many cases

- Partner’s income, for partnered claimants

There’s a free area first. Income up to a set threshold doesn’t touch your pension at all. Earn above that, and the pension drops by a published taper rate for every extra dollar of income. Keep going and you eventually hit the point where the taper has wound the pension all the way down to zero – that’s the cut-out.

Deeming is the bit that catches people out. Centrelink doesn’t ask what your savings actually earned; it assumes a return at the deeming rate. When bank interest sits below that rate, the test counts more income than your money really makes. If you’re holding a lot in low-interest accounts, that gap costs you real pension dollars.

The assets test and the family home

The assets test sweeps in most of what you and your partner own, but not everything. The big exclusion is the family home: the place you live in is exempt from the assets test no matter what it’s worth. Everything else needs checking against the table below.

| Counted as an asset | Exempt from the assets test |

|---|---|

| Investments – shares, bonds, managed funds, term deposits, savings accounts | The family home (the principal place of residence) |

| Real estate other than the family home | Some specific funeral-bond products up to defined limits |

| Vehicles, boats, caravans (above threshold values) | Certain compensation-protected categories |

| Business assets owned | |

| Some superannuation balances (varying rules by age and account type) | |

| Personal effects above defined threshold values |

One more wrinkle: homeowners and non-homeowners face different thresholds. Non-homeowners get a higher one, because the value they hold outside an exempt home is all countable. Both thresholds move with indexation over time, and the current figures live on the income-and-assets-tests page.

Payment rates, supplements, and concessions

Singles and partnered recipients are paid at different rates, and supplements lift the total a bit above the headline figure. The current numbers sit on the Age Pension rates page and are indexed twice a year, in March and September.

Three supplements usually ride alongside the pension:

- Pension Supplement – added to the basic rate

- Energy Supplement – a further small amount

- Rent Assistance – for eligible renters paying above a threshold

Then there’s the Pensioner Concession Card, which most recipients get. It cuts the cost of PBS prescriptions, public transport in many states, utility bills, and some council rates. Depending on how much you use it, that card can be worth as much as a slice of the pension itself.

How the Age Pension interacts with super

Super and the Age Pension are built to work as a pair. Super is the part you fund over your working life; the Age Pension is the floor underneath it. The link is direct – more income drawn from super reduces your pension under the means tests. The system is tuned so that plenty of people with mid-range super balances still pick up a part-pension on top of what their super pays them.

How much your super counts comes down to your age and how you’re using it:

- Below Age Pension age, super in accumulation mode is generally exempt from Centrelink means tests

- At or above Age Pension age, super balances and account-based pensions are typically counted

- Lump sum withdrawals from super that go into other assets get counted in the assets test from that point

We cover the same interaction from the super side in our superannuation eligibility article, and the bigger retirement picture is in how retirement systems work across countries, which goes into Australia in detail.

Frequently asked questions

What is the Age Pension qualifying age in Australia?

The Age Pension qualifying age is 67 for new claimants. It rose progressively from 65 over a published schedule. People born on or after 1 January 1957 reach Age Pension age at 67. Reaching the qualifying age is necessary but not sufficient — residency and means tests also apply.

Is the Age Pension means-tested?

Yes. The Age Pension uses an income test and an assets test, with Services Australia applying whichever produces the lower payment. Many people receive a part-pension rather than the full payment because their other income or assets reduce eligibility above the full-payment threshold but not below the cut-off.

Does owning my home affect Age Pension eligibility?

Owning your home doesn’t disqualify you, but it does change the assets-test thresholds. Homeowners and non-homeowners have different threshold levels because the family home itself is exempt from the assets test. Non-homeowners get a higher assets threshold to reflect the value held outside an exempt home.

The pre-retirement decision that affects Age Pension outcomes most

The decision that shapes your Age Pension the most isn’t made on the day you claim – it’s made in the years leading up to it, in how your assets and income are structured. The thresholds work in plain dollar amounts. But where those dollars sit – in super or outside it, in property or financial assets, in the family home or somewhere else – changes how they get counted against you.

Two people with the same total wealth can end up with very different pensions, simply because one understood which assets are countable and which are exempt and planned around it well before qualifying age. This isn’t about gaming anything; it’s the system doing exactly what its exemptions and rules were written to do. If you’re within five years of qualifying age and holding significant assets, this is the moment to get advice that specifically covers how the means tests treat your situation.

Use the priority order below to focus that thinking, then take it to a professional.

What matters most, in order

- Confirm the gate first. Check you’ll meet the qualifying age (67 for new claimants) and the residency rules before anything else – they’re a hard requirement, not a means test.

- Map your countable assets. List what counts (investments, non-home property, vehicles, some super) against what’s exempt (the family home, certain funeral bonds, protected compensation).

- Look at where assets sit, not just how much you have. Super versus outside super, property versus financial assets, and home versus non-home all change how the tests treat the same wealth.

- Account for deeming. Remember the income test deems a return on financial assets, which can count more income than low-interest savings actually earn.

- Don’t forget the concession card. The Pensioner Concession Card can be worth as much as a slice of the pension, so a part-pension is often worth claiming.

- Get tailored advice in the five-year run-up. This is where the means-test decisions actually get made.

The Services Australia website’s main Age Pension page stays the authoritative starting point for the rules, with rates and thresholds updated as they change.